Challenges of 35 Year Tenure KPR

Apart from the KPR scheme with a term of 35 years, there is a Tapera KPR opportunity for low-income people and millennials.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

Illustration

The Ministry of Public Works and Housing is currently developing a 35-year mortgage scheme to facilitate millennials in owning a house. This scheme is commendable, especially for millennials and low-income communities, as longer mortgage tenures result in lower monthly installments.

KPR schemes with long tenors are nothing new. Singapore, for example, through the Housing & Development Board (HBD) has mortgages with a term of up to 30 years. Australia has mortgages with tenors of up to 40 years. (Kompas, 1/24/24).

We can learn from Japan, which has a mortgage with a tenor of up to 35 years. This scheme is related to the average life expectancy of the Japanese people which reaches 84.3 years (WHO, 2023). Therefore, the mortgage should be paid off when the client is not yet 75-80 years old. Indonesian life expectancy is 73.93 years, which is 11 years less than the life expectancy of the Japanese people.

Also read: 35 Year KPR, Helping or Burdening?

KPR interest rates Japan is also very low. The average mortgage fixed interest rate in 2014-2023 is "only" 3.53 percent at top banks. This figure is above Japan's benchmark interest rate of minus 0.10 percent.

What is the Base Credit Interest Rate (SBDK) for KPR in Indonesia? The prime lending rate as of November 2023 at 10 large banks can be used as a reference, namely Bank Mandiri (7.30 percent), BRI (7.25 percent), BCA (7.20 percent), BNI (7.30 percent), BTN (7, 30 percent), CIMB Niaga (7.30 percent), Bank Danamon (8 percent), Bank Permata (8.58 percent), OCBC NISP (8 percent), and Bank Panin (8.05 percent).

The Basic Credit Interest Rate does not include risk premium (risk premium). The risk premium represents the bank's assessment of the prospects for credit repayment by prospective debtors which, among other things, considers the debtor's financial condition, credit term, and prospects of the business being financed.

This means that the prime lending rate is not the same as the KPR interest rate. The prime lending rate plus the new risk premium will become the KPR interest rate. Because of this, floating interest rates (floating rates) for mortgages can reach 13 percent.

SBDK has not been effective in reducing high KPR interest rates so that they are more affordable for millennials and MBR.

A floating interest rate is an interest rate that follows changes (up or down) in the BI benchmark interest rate (7 Day Reverse Repo Rate) which has now reached 6 percent. On the other hand, a fixed interest rate is an interest rate that does not change when the BI benchmark interest rate changes.

Therefore, the home ownership loan interest rate in Indonesia is much higher than BI's benchmark interest rate. Furthermore, compared to Japan's average fixed home ownership loan interest rate of 3.53 percent, it is even higher.

This suggests that SBDK has not been powerful enough to reduce high mortgage interest rates so that they become more affordable for millennials and low-income families. This is a serious challenge for the Financial Services Authority (OJK) and national banks.

A row of new houses in Cibunar, Parung Panjang District, Bogor Regency, West Java, on Thursday (19/1/2023). Hundreds of houses built in this location are government-subsidized houses with a mortgage scheme.

Alternative solution

The 35-year Home Ownership Credit will be hampered by regulations stating that the Building Use Rights Certificate (SHGB) is only valid for 30 years (bisnis.com, 25/1/24). What are the alternative solutions?

Therefore, the tenure for a mortgage is limited to 30 years. However, in the 10th year, the tenure may be reduced to 20 years, for example. This is applied under the assumption that the customer's salary has increased. Consequently, monthly installments become higher. The purpose of shortening the tenure is to provide customers with the opportunity to be able to pay for other installments, such as for motor vehicles.

However, there is a tendency for millennials to like to travel abroad even by paying in installments using paylater or digital wallets, such as i.saku, Shopee Pay, Linkaja, OVO , DANA, DOKU, and Gopay. Remember that high interest installments can catch your neck!

The 35-year Home Ownership Credit (Kredit Kepemilikan Rumah) will be hindered by the regulation that the Building Usage Rights Certificate (SHGB) provision is only for 30 years.

There is another tip, namely with tiered interest rates, initially with a fixed interest rate for 15 years. Then continued with floating interest rates for 15 years because customer salaries were getting higher.

In truth, even before the emergence of the 35-year mortgage scheme discourse, the housing finance liquidity facility program (FLPP) or subsidized mortgage program specifically for low-income households earning a maximum monthly income of Rp 8 million was already available.

What are the advantages of FLPP mortgages? A down payment of up to 1 percent, a fixed interest rate of 5 percent until the 20-year tenor is paid off. FLPP mortgages already include life insurance premiums, fire insurance, and credit insurance. FLPP mortgages are exempt from 11 percent value-added tax (VAT).

The affordable housing mortgage program (KPR FLPP) is managed by the People's Housing Savings Management Agency (Tapera) in accordance with Law Number 4 of 2016 and Government Regulation (PP) Number 25 of 2020 regarding Tapera.

The conditions for a subsidized housing loan (KPR FLPP) to become a Tapera participant are that they must be a civil servant, military/police personnel, formal worker, or self-employed worker. Employers are required to register their employees, while self-employed workers can register themselves.

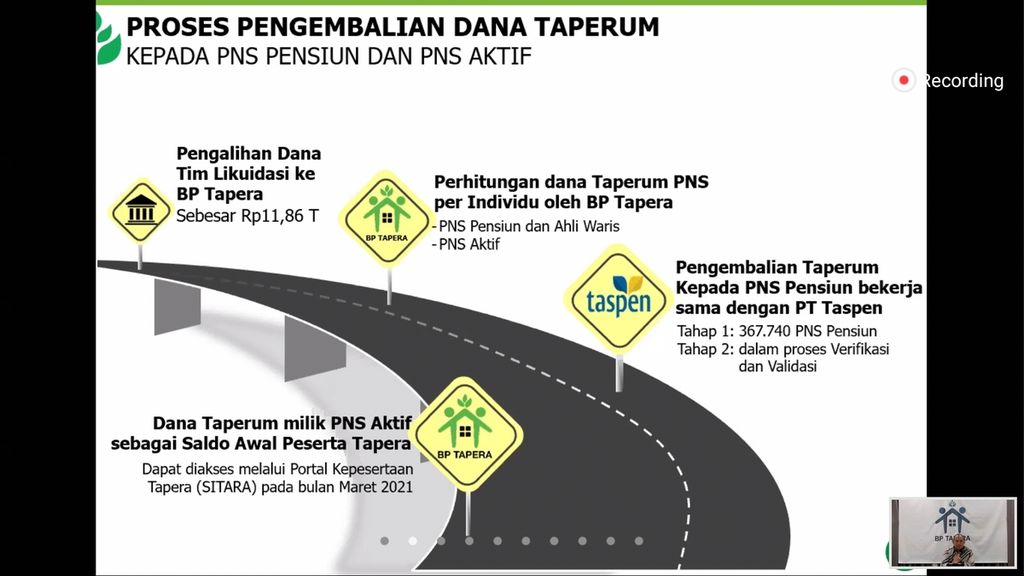

Exposure from BP Tapera in a virtual press conference regarding the return of Taperum funds for retired civil servants or their heirs, on Tuesday (19/1/2021).

The government will cut the FLPP KPR tenor from 20 years to 10 years starting in 2025. In this case, the FLPP KPR tenor can remain up to 20 years, but the subsidy is only 10 years and after that the interest rate will be reviewed. If customers can afford it, they will be charged a floating interest rate (Kompas, 16/2/24). Don't let this idea aim to prioritize 35 year mortgages.

The plan to cut the tenor could be an obstacle for the marketing of FLPP mortgages. This scheme becomes less attractive. Moreover, in 2027, BP Tapera must not only collaborate with Tapera participants from ASN and TNI/Polri, but also participants from the private sector (formal workers) and independent workers.

Currently, the price of subsidized houses (KPR FLPP and KPR Tapera) has increased. This is stated in the Minister of Public Works and Public Housing Decision Number 689/KPTS/M/2023 regarding the Limitations on Land Area, Floor Area, and Selling Price Limitations for Public Housing in the Implementation of FLPP Housing Credit/Financing and the Amount of Subsidy for Housing Down Payment Assistance (SBUM).

Also read: Government Examines 35 Year Fixed Interest Mortgage Scheme

The regulations set a limit on the selling price of houses, divided into five regions. The lowest subsidized house price is Rp 166 million starting from January 2024 in Java (excluding Jakarta, Bogor, Depok, Tangerang, Bekasi) and Sumatra (excluding Riau Islands, Bangka Belitung, Mentawai Islands).

In Kalimantan (excluding Murung Raya Regency and Mahakam Ulu Regency), house prices are at Rp 182 million. In Sulawesi, Bangka Belitung, Mentawai Islands, and Riau Islands (excluding Anambas Islands), house prices are at Rp 173 million. The highest house price is at Rp 240 million in Papua, West Papua, Central Papua, Papua Mountains, Southwest Papua, and South Papua.

Therefore, in addition to the 35-year tenor mortgage scheme, it is highly commendable for the Ministry of PUPR to encourage MBRs as well as millennials to adopt FLPP mortgages or Tapera mortgages managed by BP Tapera. Moreover, the Minister of PUPR serves as the Chairman of the Tapera Committee or the "boss" of BP Tapera.

Paul Sutaryono, Banking Observer; Assistant Vice President BNI (2005-2009); UPDM Center for Business Studies (PSB) Expert Staff

Paul Sutaryono